Gold stocks are still on a tear, and Agnico Eagle Mines (NYSE: AEM) has been one of the biggest beneficiaries.

With gold prices hitting fresh highs and investors piling into producers with scale and stability, the company’s shares have climbed sharply over the past couple of years.

The question now isn’t whether the company is executing. It’s whether the stock price already reflects that success.

Agnico Eagle is one of the world’s largest gold miners, operating primarily in Canada, Australia, Finland, and Mexico. Its asset base includes the Detour Lake and Canadian Malartic mines (the two largest gold mines in Canada) and is supported by a deep pipeline of expansion projects.

The company’s most recent results were strong.

It produced 3.45 million ounces in 2025 and is targeting stable annual production between 3.3 million and 3.5 million ounces through 2028, with a longer-term path toward more than 4 million ounces annually in the early 2030s.

In the fourth quarter, the company produced 841,000 ounces at total cash costs of $1,089 per ounce and all-in sustaining costs, or AISC, of $1,517. For the full year, total cash costs were $979 per ounce and AISC was $1,339.

Adjusted earnings for the year reached $4.2 billion, and free cash flow came in at $4.4 billion. The balance sheet improved meaningfully, with roughly $950 million in debt repaid and cash rising to about $2.9 billion.

Management also increased the quarterly dividend by 12.5% to $0.45 (which comes out to a 0.73% annual yield) and expanded its buyback authorization.

That operational strength brings us to valuation.

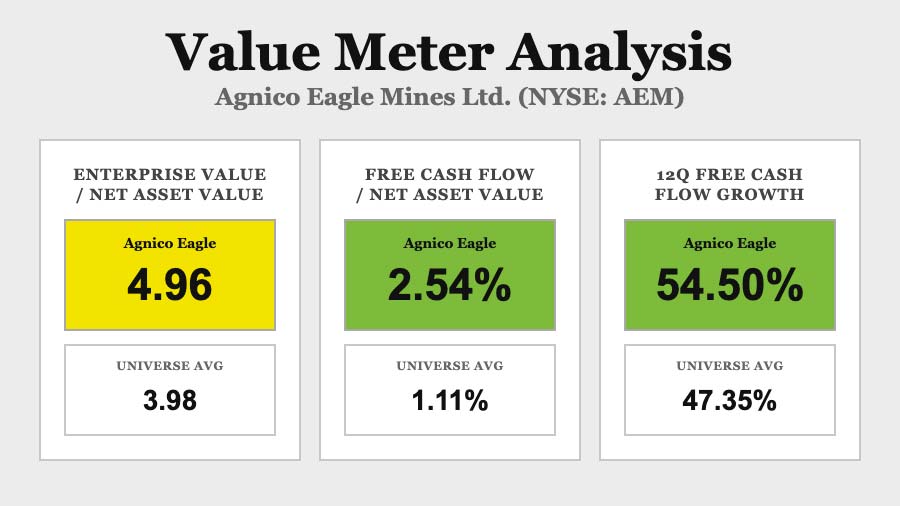

Agnico Eagle trades at an EV/NAV of 4.96, versus a universe average of 3.98. This tells us investors are paying a premium for each dollar of net asset value compared with the company’s peers.

That premium suggests the market views Agnico Eagle’s asset base as higher-quality and lower-risk than the average miner’s.

The company looks stronger on a cash-efficiency basis as well. Its FCF/NAV is 2.54%, versus 1.11% for the broader universe. Agnico Eagle is converting its assets into free cash flow more than twice as efficiently as the average company.

That helps justify part of the valuation premium.

Growth adds another layer. Over the past 12 quarters, free cash flow has grown quarter over quarter 54.5% of the time, surpassing the broad average of 47.35%.

While not dramatically higher, that does show that Agnico Eagle is expanding its cash generation faster than the typical company in its group.

The company combines scale, disciplined cost control, and a visible production growth pipeline.

Still, the stock is no longer a bargain. Much of the operational upside appears to already be reflected in the price.

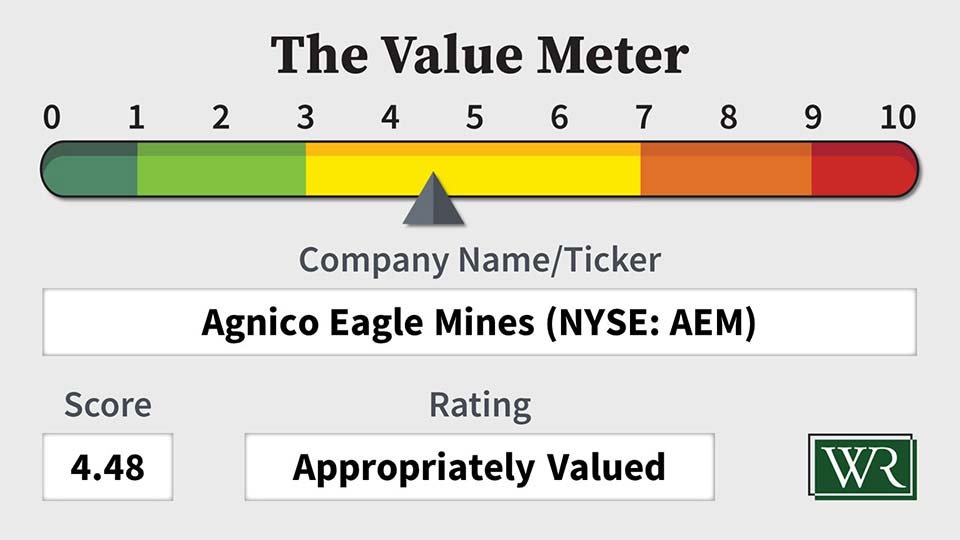

The Value Meter rates Agnico Eagle Mines as “Appropriately Valued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.

{kind=link}