In late 2023, mortgage real estate investment trust Arbor Realty Trust (NYSE: ABR) received a “B” for dividend safety.

At the time, the only issue was that net interest income (the measure of cash flow used by mortgage REITs) was expected to fall in 2024.

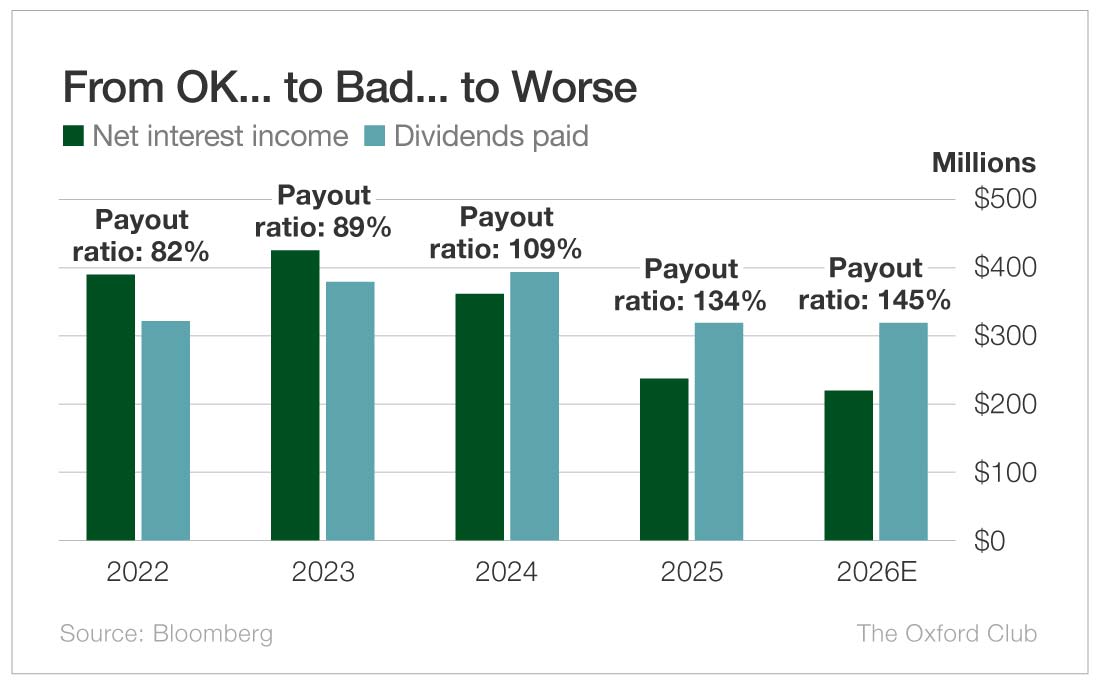

In March of 2025, I reviewed Arbor again, and its dividend safety rating deteriorated to a “C” because the company had paid out more in dividends than it made in net interest income in 2024 and was expected to do the same in 2025.

At its current price, the stock yields more than 13%. In the year since we last reviewed it, did Arbor’s dividend safety rating improve… or topple like an aged redwood?

Last year, Arbor’s net interest income plummeted from $363 million to $238 million. (It had been expected to rebound to $409 million.)

Meanwhile, it paid out $320 million in dividends for a payout ratio of 134%.

In other words, it paid out $1.34 for every $1 it took in.

That’s bad.

For REITs, including mortgage REITs, I’m fine with payout ratios of 100% or lower.

By law, REITs must pay out 90% of their net income in dividends in order to avoid corporate tax on it.

Keep in mind, net interest income is different from net income. There are other items included in net income that aren’t part of net interest income. (In Arbor’s case, net income is even lower than net interest income.)

As a result, if you look on many of the free websites, you’ll see payout ratios that are significantly different from mine, because they incorrectly use net income instead of net interest income (or, for non-REITs, free cash flow) to calculate the payout ratio.

Because of the law that these companies must pay out nearly all of their profits in dividends, I’m comfortable with a payout ratio of up to 100% − but not more. Once it’s over 100%, that means the company is paying more in dividends than it is making in cash. The only ways it can afford its dividend in that case are burning through cash, selling shares, or taking on debt to raise cash, none of which are sustainable.

This year, net interest income is projected to slip again to $220 million, and dividends paid are forecast to remain at $320 million for an even more strained 145% payout ratio.

If all that isn’t rough enough, Arbor has cut its dividend twice in the past year.

After eliminating its dividend during the global financial crisis, Arbor reinstated its payout in 2012 and raised it every year until last year.

Then, in the second quarter of last year, the quarterly dividend was cut from $0.43 to $0.30. In May, the company slashed it again − all the way down to $0.17, back to the same level it was in March of 2017.

Arbor’s dividend is not safe.

Dividend Safety Rating: F

What stock’s dividend safety would you like me to analyze next? Leave the ticker in the comments section.

You can also take a look to see whether we’ve written about your favorite stock recently. Just click on the word “Search” at the top right part of the Wealthy Retirement homepage, type in the company name, and hit “Enter.”

Also, keep in mind that Safety Net can analyze only individual stocks, not exchange-traded funds, mutual funds, or closed-end funds.

The post Arbor Realty Trust: How Sturdy Is Its 13% Yield? appeared first on Wealthy Retirement.

{kind=link}