Despite pressures from renewable energy transitions, coal remains a critical resource for both power generation and steel production. Peabody Energy, the largest coal mining company in the United States, stands out as a compelling investment opportunity on this field. With a robust operational footprint, strong financial metrics, and a valuation that suggests significant upside, Peabody offers a unique blend of stability and growth potential.

Company Overview and Market Position

Founded in 1883 and headquartered in St. Louis, Missouri, Peabody Energy is a global leader in coal production, operating 17 coal mines across the United States and Australia. Its flagship asset, the North Antelope Rochelle Mine in Wyoming’s Campbell County, is one of the world’s largest coal mines, producing over 60 million tons annually, primarily thermal coal for electricity generation.

In the U.S., Peabody’s operations span Alabama, Colorado, Illinois, Indiana, and New Mexico, employing both surface and underground mining techniques. In Australia, its Queensland and New South Wales mines, including the recently restarted Centurion Mine, focus on metallurgical coal for steelmaking, a segment showing resilience amid global demand from Asia.

Peabody ranks among the top five global coal companies, alongside giants like China Shenhua, Coal India (NSE:), Glencore (OTC:), and Anglo American (JO:). It supplies coal to over 26 countries, with 55-63% of its revenue derived from international markets, particularly Asia (China and India being key buyers).

The company’s diversified portfolio-spanning thermal coal for energy and metallurgical coal for steel-positions it to capitalize on varying demand dynamics. Notably, its seaborne metallurgical mining segment, which involves mining, enrichment, and maritime transport, has shown stable reserve growth in 2024, even as overall proven reserves decline industry-wide.

Financial Health: A Case for Undervaluation

Peabody’s financial metrics paint a picture of a fundamentally strong, but yet undervalued company at the same time. Let’s take a look at its key indicators, step by step:

Price-to-Earnings (P/E) Ratio: 6.5, significantly below the coal industry average of 9.04, suggesting a 40% discount to peers. With an earnings per share (EPS) of $1.96, this implies a fair value of approximately $17.72, offering over 40% upside from the current price of $14.61.

Dividend Yield: 2.4%, modest but stable, with payouts consuming just 11.4% of profits, leaving ample room for reinvestment or future increases.

- Price-to-Book (P/B) Ratio: 0.42, indicating the stock trades at less than half its book value-a pretty rare bargain in the sector.

- Price-to-Sales (P/S) Ratio: 0.4, reflecting a market capitalization ($1.54 billion) that is only 40% of annual revenue ($4.24 billion), a sign of deep undervaluation.

- Enterprise Value-to-EBITDA (EV/EBITDA): 1.7, among the lowest in the industry, highlighting operational efficiency relative to its $1.37 billion enterprise value.

- Debt Metrics: A debt-to-assets ratio of 7.8% and debt-to-equity ratio of 12.8% reflect minimal leverage, while EBITDA covers interest expenses 9.5 times, signaling financial resilience.

- Cash Flow: A price-to-cash-flow ratio of 2.6 indicates the business is priced at just 2.6 times its annual cash flow, with $205.2 million in free cash flow supporting dividends and growth initiatives.

Such metrics underscore Peabody’s ability to generate strong returns-10.5% operating margin, 10.5% net margin, 11.1% return on equity (ROE), and 10.3% return on assets (ROA)-while maintaining a lean balance sheet. The company’s liquidity is robust, with a current ratio of 2.2, ensuring it can meet short-term obligations comfortably.

Coal Industry Dynamics: Challenges and Opportunities

Peabody’s performance is closely tied to global coal prices, which have faced headwinds in 2024-2025. Thermal coal, used for electricity, trades at approximately $95 per ton, while metallurgical coal, critical for steel production, fetches $183 per ton.

Production costs vary: U.S. thermal coal costs $10-20 per ton, while Australian metallurgical coal ranges from $60-90 per ton. Despite these margins, Peabody’s revenue has declined due to softer prices, which goes straight from reduced European demand for thermal coal (amid renewable energy shifts, EU, for example) and lower Chinese imports. However, 2025 shows signs of stabilization, with prices supported by supply constraints in Australia, growing demand in India and Southeast Asia, and persistent energy needs in developing economies.

The coal industry faces long-term challenges, including regulatory pressures in the U.S. and Australia over environmental concerns and a gradual decline in thermal coal demand in developed markets. Yet, recent events-such as blackouts in Spain and Portugal linked to overreliance on renewables-highlight coal’s enduring role as a reliable energy source.

Renewable energy exceeding 15% of a grid’s capacity can lead to instability, suggesting thermal coal may see renewed demand in the coming decade. Metallurgical coal, less affected by green transitions, benefits from steady steel demand, particularly in Asia.

Peabody’s strengths-low debt, high profitability, diversified operations, and strong cash flow-position it to weather and overcome this kind of challenges. Its weaknesses, namely exposure to volatile coal prices and regulatory risks, are mitigated by its global reach and operational efficiency. The industry’s underinvestment in new coal deposits over recent decades, coupled with depleting reserves (Peabody’s proven reserves stood at 2.4 billion tons for 2022 year), could tighten supply and drive prices higher, further enhancing Peabody’s prospects.

Investment Thesis and Recommendation

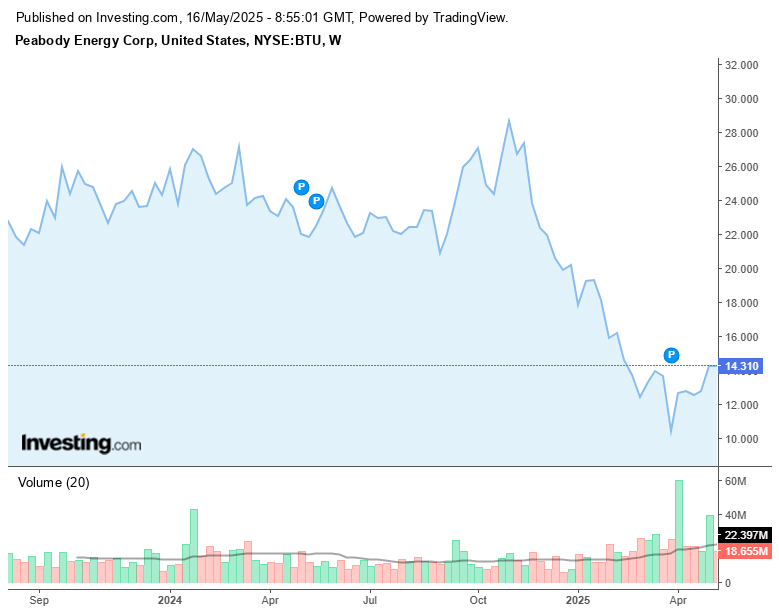

Peabody Energy offers a rare combination of value and resilience in a misunderstood sector. Trading at $14.61, its stock is undervalued by nearly 40% relative to the industry’s average P/E, with a fair value of $17.72 based on current earnings. This discount persists despite stable coal prices and Peabody’s operational strength, suggesting market skepticism about coal’s future is overblown.

The company’s minimal debt, high cash flow, and diversified revenue streams (55-63% from exports) provide a buffer against market volatility, while its 2.4% dividend yield adds income appeal.

Upside catalysts include potential coal price rebounds, particularly if global energy demand outpaces renewable capacity, and continued growth in Asian steel production. Risks include further regulatory tightening and price volatility, but Peabody’s low valuation and strong balance sheet offer a margin of safety. Analyst consensus supports this view, with a price target of $27.60 (88,9% above current levels) and a “Strong Buy” rating.

Recommendation: Very Positive

Peabody Energy is a compelling value play for those investors who are looking for exposure to the coal sector’s rebound potential. Its undervaluation, financial discipline, and strategic positioning make it a standout choice in a market ripe for reassessment.

{kind=link}