America’s power grid has a simple problem: Demand is rising, and reliable supply is not easy to add overnight.

That is why power players like Vistra (NYSE: VST) − one of the largest power generators in the U.S., with enough capacity to power about 22 million homes − matter.

Vistra operates in all of the major power markets across the country, and its fleet spans natural gas, nuclear, coal, solar, and battery energy storage. It also runs the second-largest competitive nuclear fleet in the U.S.

Investors in Vistra aren’t just paying for the usual power story. They are paying for scale, reliability, and cash flow.

But are they paying too much?

After a huge two-year run, the stock has cooled. Buyers have looked more selective than excited in recent months. That fits the facts: The business is still producing strong cash, but the stock price is already giving it a lot of credit.

In other words, the issue is not whether Vistra is doing well. It’s whether the stock is giving new buyers enough value.

In the first quarter of 2026, Vistra reported revenue of $5.6 billion, up 43% from $3.9 billion a year earlier. Net income was $1 billion, against a net loss of $268 million in the first quarter of 2025. Operating cash flow rose from $599 million to $1.2 billion while ongoing operations adjusted EBITDA, a profit measure that excludes interest, taxes, and some noncash items, grew to $1.5 billion.

Let’s see how those numbers stack up with our Value Meter metrics.

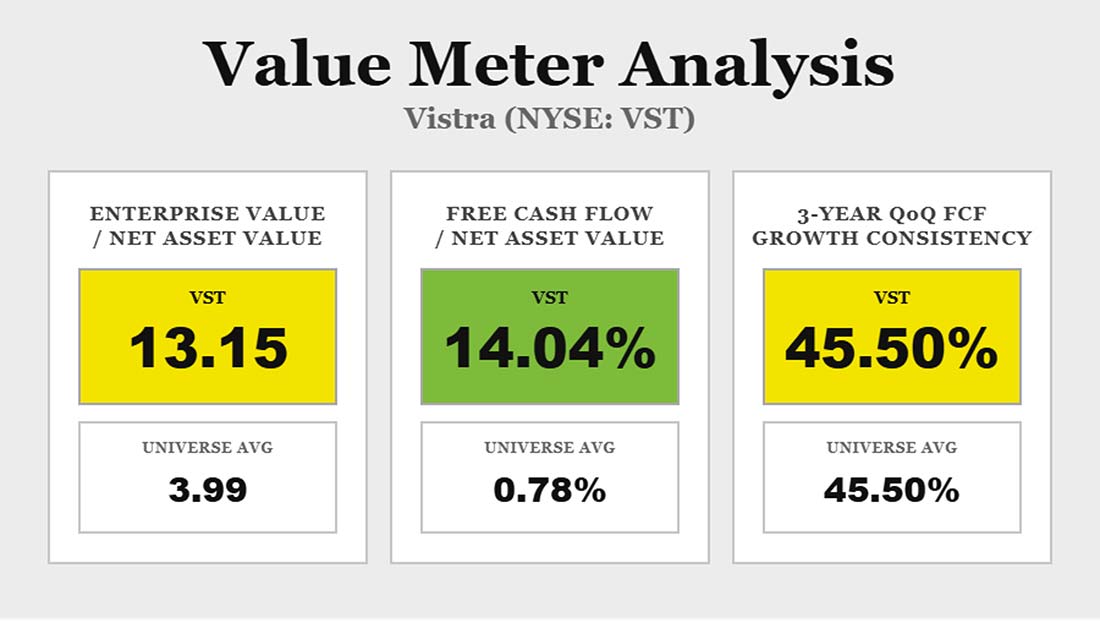

Vistra’s enterprise value-to-net asset value (EV/NAV) ratio is 13.15, versus the broad market average of 3.99. That’s a premium of about 229% above the market.

Free cash flow-to-net asset value (FCF/NAV), which compares the company’s remaining cash after spending with its asset value, is much stronger. Vistra’s FCF/NAV is 14.04%, versus the broad market average of 0.78%. That is 1,708% higher than the average company. This shows that the premium is backed by a large stream of cash.

Vistra’s three-year quarter-over-quarter free cash flow growth consistency is 45.5%, the same as the broad market average. That means free cash flow has grown from the prior quarter nearly half of the time. The cash is strong, but the pattern is no more consistent than the broader market’s.

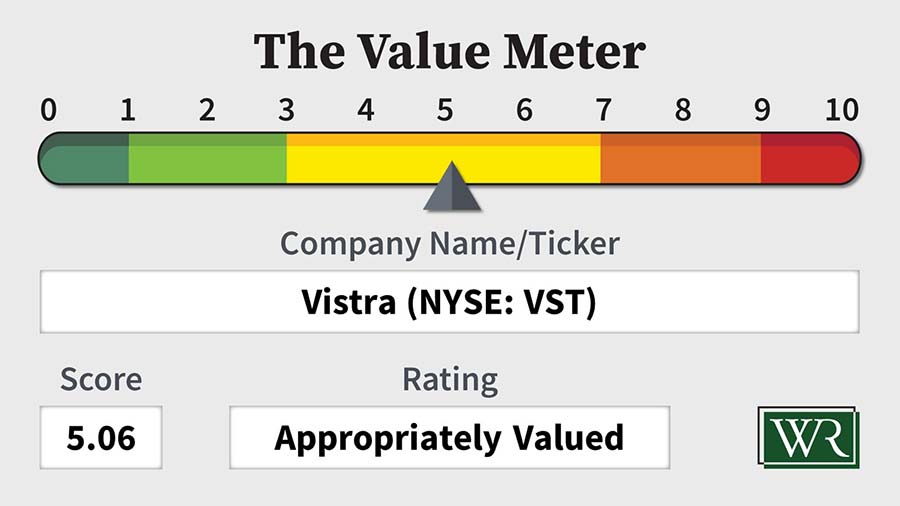

The market appears to be assuming that Vistra can keep turning power demand and solid fundamentals into strong cash flow. The data supports much of that view, but it does not support a low Value Meter rating. The company’s cash flow is far better than average, while its asset valuation is far more expensive than average. That leaves the stock in a fair zone, not a cheap one.

The Value Meter rates Vistra as “Appropriately Valued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.

{kind=link}