I’ve always been amazed by the story of nuclear power.

Decades ago, it promised a future with less need for oil and gas. Then nuclear technology became linked to war, and the accident at Three Mile Island turned public sentiment strongly against it.

Now nuclear power is back. Its future looks brighter.

However, the next nuclear age could look very different. Huge plants may give way to smaller reactors built near their customers.

Oklo (NYSE: OKLO) is developing small nuclear plants called Aurora powerhouses. It plans to build, own, and run them, then sell power and heat. It is also working on nuclear fuel and medical isotopes.

The appeal is easy to see. Power use is rising, data centers need steady electricity, and nuclear energy has fresh political support.

But interest is not profit.

In the first quarter of 2026, Oklo posted a net loss of $33.1 million and an operating loss of $51.2 million. It used $17.9 million in cash to run the business, and it spent $32.8 million on plants and equipment.

On the other hand, Oklo earned $21.3 million from interest and dividends on its large cash pile, which helped cut the net loss.

The company ended the quarter with $2.5 billion in cash and investments. That gives it time to build. But most of the gain came from selling new shares, not from the business itself.

The stock rose fast, then gave back some gains over the past year, but the fall has stopped for now. Investors seem unsure. They aren’t sold, but they have not left.

That caution fits the facts. Oklo is making real progress. Yet its price still rests on plants, sales, and cash that may come later.

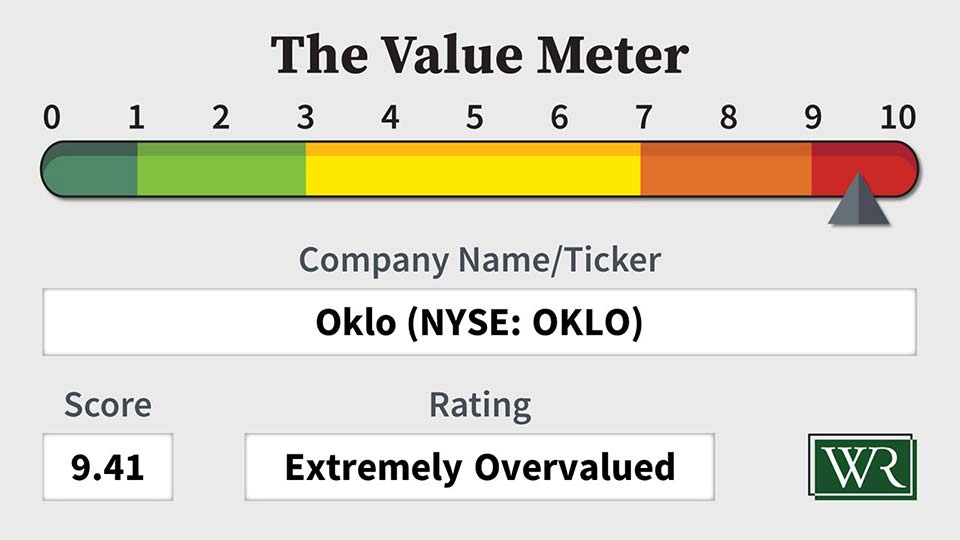

Are investors paying a fair price for the company? That’s what The Value Meter is designed to answer. Let’s run Oklo through it.

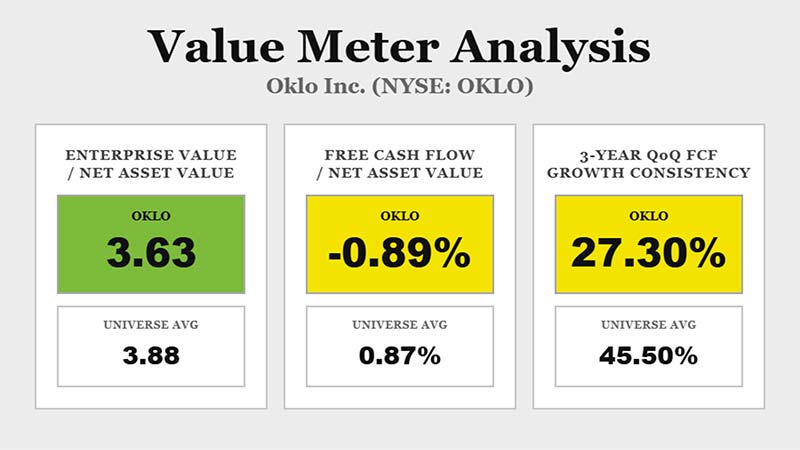

EV/NAV compares the company’s total value with its net assets. At first glance, Oklo looks fair on this test. Its EV/NAV is 3.63 − 6% below the broad market average of 3.88. However, many of its assets are still being built. They do not yet produce steady cash.

The cash test is much worse.

FCF/NAV compares free cash flow with net assets. Over the past 12 months, Oklo’s figure is -0.89%. The broad market average is 0.87%. In other words, Oklo’s assets currently burn cash. The average company produces it.

Cash flow has also lacked a steady pattern. Over the past three years, quarterly free cash flow rose from the prior quarter just 27.3% of the time. The broad market average was 45.5%.

So even when Oklo’s cash flow gets better, it may not be often enough to support a strong value case in the near future.

Oklo may become an important nuclear company, but the stock is asking investors to pay today for results that may take years to arrive.

The Value Meter rates Oklo as “Extremely Overvalued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.

{kind=link}