Inflation remains a sticking point for American shoppers. We’ve come a long way from the eye-popping 9% peak of a few years ago, but prices are still not where the Federal Reserve wants them.

With energy prices moving higher as tensions with Iran shake the oil market, consumers have little reason to feel more at ease. Household budgets are still tight. Food, rent, debt payments, and gas all compete for the same paycheck. Many families are constantly having to decide where to shop and what to skip.

That is where department stores like Kohl’s (NYSE: KSS), which runs more than 1,100 stores in 49 states, come into play. The company sells clothes, shoes, accessories, beauty products, home goods, and other family items. Its stores remain the core of the business, while online sales and the Sephora “shop-in-shop” deal help bring in traffic.

The industry backdrop has not been pretty. Department stores have lost ground for years as shoppers have shifted more spending toward online retailers, off-price chains, and brands that sell direct.

That puts Kohl’s in a tough spot.

In the first quarter of fiscal 2026, which ended in early May, Kohl’s reported total revenue of $3.17 billion, down from $3.23 billion a year earlier. Net sales fell 1.7% from $3.05 billion to $3 billion, while comparable sales (sales at stores that had been open for at least a year) fell 1.1%.

The company lost $14 million overall, compared with a loss of $15 million in the same quarter last year. Operating cash flow was -$74 million, versus -$92 million in 2025.

Kohl’s has a large store base, a known brand, and a beauty partnership that can bring in younger shoppers, but market sentiment remains cautious. Investors appear open to a turnaround, yet they are not treating the stock like a healthy growth story.

That being said, the market is less negative than it was. The stock still carries the mark of a long decline, but recent trading shows buyers are willing to give the turnaround more time.

That view only partly fits the numbers, since sales are still lower and cash flow is still negative.

The issue is not whether Kohl’s has improved at the margin. It has. The issue is whether the price is low enough to make up for a business that still has work to do.

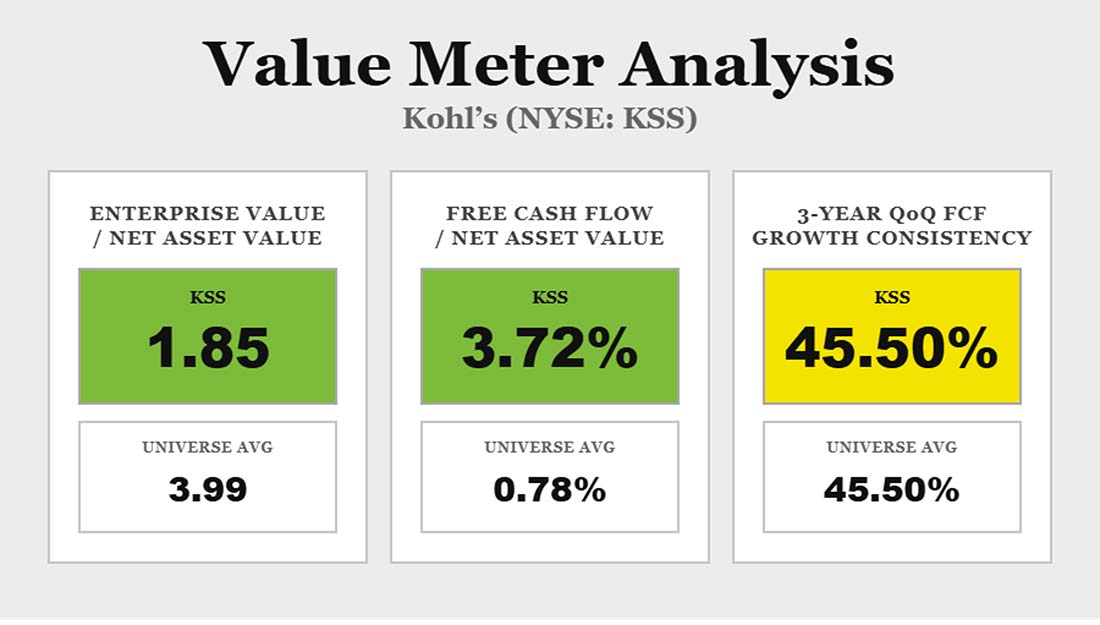

Kohl’s enterprise value-to-net asset value (EV/NAV) ratio is 1.85. That is about 54% lower than the broad market’s 3.99, which means the market is paying much less for each dollar of assets.

The company’s free cash flow-to-net asset value (FCF/NAV) percentage is 3.72%, versus the broad market average of 0.78%. That’s about 379% higher than the market average. Free cash flow could fade fast if sales keep sliding, but this gives the value case real support.

Kohl’s quarterly free cash flow has grown from the prior quarter 45.5% of the time over the past three years. That matches the broad market average. The company’s cash flow efficiency may be strong, but the cash flow pattern is not better than average.

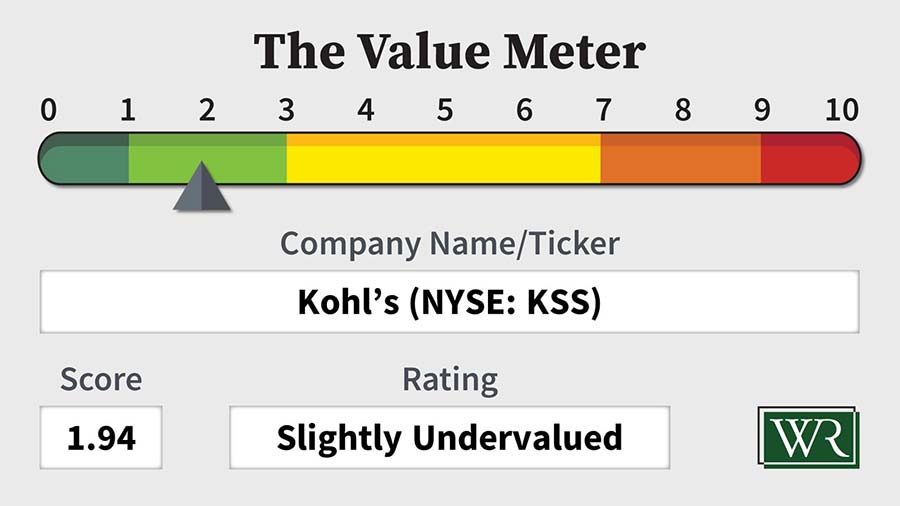

The market seems to be saying Kohl’s may be past the worst of its decline. The Value Meter data is more cautious. The stock is cheap, and the company is converting its assets into cash at a solid clip, but the business has not yet shown steady growth, firm sales, or clear cash flow strength.

This is not a clean bargain, but the price does reflect a lot of bad news.

In other words, there are clear reasons the stock is cheap, but it may still be slightly attractive here.

The Value Meter rates Kohl’s as “Slightly Undervalued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.

{kind=link}