Sometimes it’s hard to shake your history.

Rolling Stones guitarist Keith Richards hasn’t done hard drugs in decades. These days, you’ll find him tending to his garden or doting on his grandchildren, but I’m sure when you think about “Keef,” this is closer to the image you have of him.

Armour Residential REIT (NYSE: ARR), a real estate investment trust that invests in mortgages backed by the U.S. government, is in a similar situation. Its past is hard to forget.

However, the company’s financials are in decent shape.

Last year, it generated $297 million in distributable earnings, the measure of cash flow the company uses. That was a big improvement over 2024’s $189 million.

This year, the mortgage REIT is expected to achieve $336 million in distributable earnings, and that figure is projected to continue climbing for at least the next two years.

In 2025, Armour paid shareholders $272 million in dividends, or 92% of its distributable earnings.

I’m fine with REITs paying out as much as 100% of their cash flow in dividends. By law, they must pay 90% of their net income in dividends in order to avoid corporate taxes, so their payout ratios are typically higher than those of regular companies.

The payout ratio is projected to decline to under 91% in 2026.

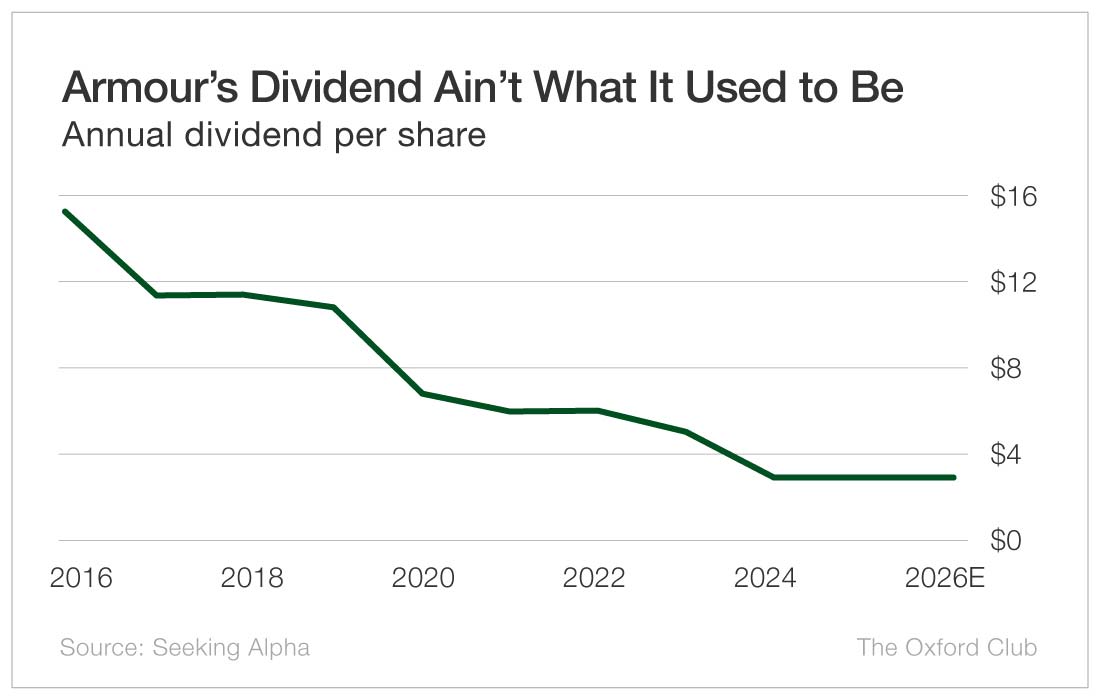

The problem is Armour Residential REIT has been a serial dividend cutter.

It hasn’t lowered the dividend in 2 1/2 years, but before that, reductions were a regular occurrence.

Over the past 10 years, management reduced the dividend six times.

In fact, the dividend per share is 85% lower than it was at the start of 2016.

That being said, the $0.24 per share monthly dividend still comes out to an impressive 17% yield.

The company also regularly sells shares. In 2016, there were 7.3 million shares outstanding. Today there are 105.3 million.

That constant increase in the share count means the company must continue to boost distributable earnings. Otherwise, it won’t be able to cover the dividend. There isn’t much margin for error.

Armour Residential REIT can afford its dividend right now, and with distributable earnings expected to grow, it should be able to in the near term.

However, its dividend-cutting track record means you can never really rely on the payout until management has proven over a longer period that it won’t be so quick to pull the trapdoor on its dividend.

Armour Residential’s dividend-cutting reputation is hard to shake.

Dividend Safety Rating: F

What stock’s dividend safety would you like me to analyze next? Leave the ticker in the comments section.

You can also take a look to see whether we’ve written about your favorite stock recently. Just click on the word “Search” at the top right part of the Wealthy Retirement homepage, type in the company name, and hit “Enter.”

Also, keep in mind that Safety Net can analyze only individual stocks, not exchange-traded funds, mutual funds, or closed-end funds.

{kind=link}