I get a lot of requests to analyze the dividend safety of AGNC Investment Corp. (Nasdaq: AGNC). It’s not surprising that it’s popular given its 14% yield.

I’ve looked at AGNC several times. In October of last year, I gave it an “F” rating for dividend safety.

In January of 2024, I said AGNC had “as bad a dividend history as I’ve seen.” At that time, it had cut its dividend nine times in 12 years.

However, the dividend has stabilized. It’s remained at $0.12 per share monthly since April 2020.

Whether the company can actually afford to pay its dividend is another question.

AGNC is a mortgage real estate investment trust, or REIT. It borrows money for the short term and invests in mortgages over the longer term.

The cash flow metric used by mortgage REITs is net interest income − the difference between what they pay to borrow the money and what they earn from their mortgage investments (minus expenses).

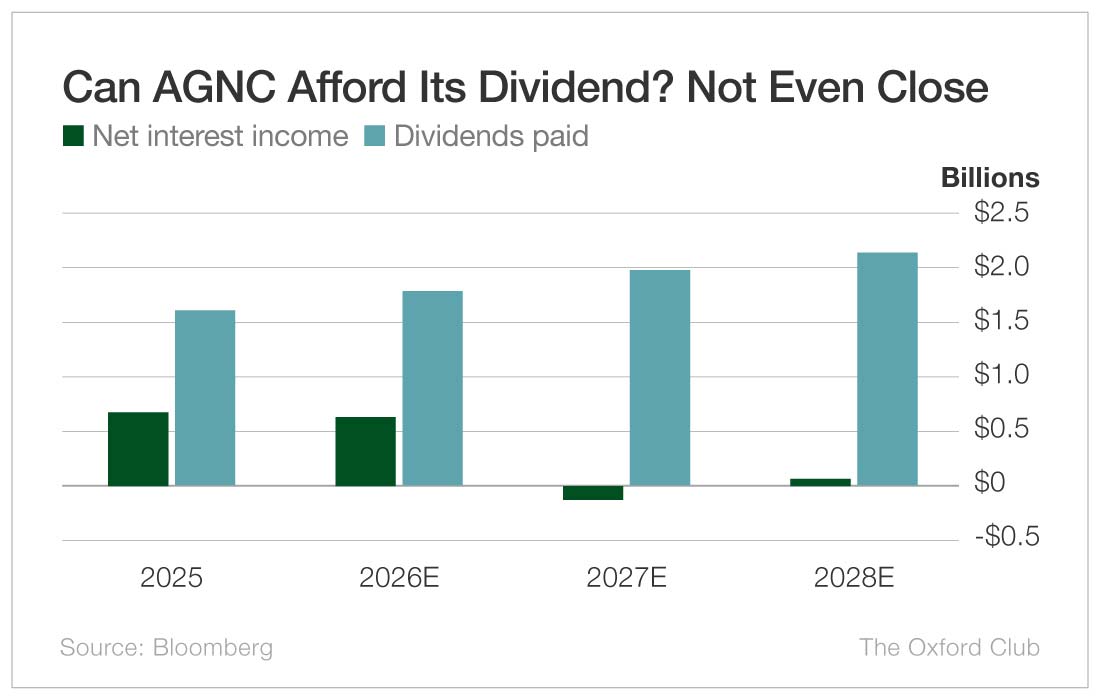

In 2025, AGNC generated $675 million in net interest income while paying shareholders $1.6 billion in dividends. You don’t need a Ph.D. in math to realize it is paying investors more than it makes.

If you make $675 a week and pay $1,600 in expenses, you’ll be in a hole pretty fast.

This year, the situation is not likely to get any better.

Net interest income is forecast to dip to $637 million, while dividends paid are expected to be nearly $1.8 billion.

The Safety Net model doesn’t take projections beyond the current year, but it’s worth noting that expectations for 2027 and 2028 are miserable.

Net interest income is forecast to go negative next year and then barely climb back above breakeven in 2028.

Meanwhile, dividends paid will continue to rise − not because of a dividend hike, but because the company constantly issues new shares to raise money to afford the dividend.

In fact, it has doubled its number of shares outstanding since 2022 and tripled it over the past 10 years.

AGNC doesn’t come close to making enough net interest income to pay shareholders the current dividend. In the past, it has had to sell shares to raise cash in order to afford its payout. It will have to continue to do so in order to pay the current dividend, fueling the cycle of higher dividends paid.

Remember, that’s total dividends paid, not dividends per share. Shareholders aren’t receiving more income. The company is paying out the same dividend per share across more shares.

Something has to give. Eventually, management will have to go back to doing what it did in the last decade and slash the dividend significantly. It cannot continue on the same trajectory it’s on now.

It’s simple math.

Dividend Safety Rating: F

What stock’s dividend safety would you like me to analyze next? Leave the ticker in the comments section.

You can also take a look to see whether we’ve written about your favorite stock recently. Just click on the word “Search” at the top right part of the Wealthy Retirement homepage, type in the company name, and hit “Enter.”

Also, keep in mind that Safety Net can analyze only individual stocks, not exchange-traded funds, mutual funds, or closed-end funds.

{kind=link}