Industrial stocks rarely generate the kind of excitement seen in technology or biotech. Yet when sentiment around a long-established manufacturer turns cautious, patient investors sometimes find opportunity.

That appears to be the case with Stanley Black & Decker (NYSE: SWK), whose shares have struggled in recent years as the company worked through restructuring efforts and shifting demand in the tools market.

Chief Income Strategist Marc Lichtenfeld took a look at the company on Wednesday in his Safety Net column, where he evaluates the safety of companies’ dividends. He gave it a “B” grade, indicating a low risk of the dividend being cut.

But Safety Net and The Value Meter use different criteria. A safe dividend doesn’t necessarily imply an attractive valuation.

Stanley Black & Decker is one of the world’s best-known toolmakers, with a portfolio that includes iconic household brands like DeWalt, Craftsman, Stanley, and Black+Decker.

The company sells professional and consumer tools, outdoor equipment, and industrial fastening systems across global markets. Its products are staples for contractors, manufacturers, and DIY enthusiasts alike, giving it a broad and durable customer base.

The company’s most recent results show a business stabilizing after a challenging period. In the fourth quarter of 2025, Stanley Black & Decker generated $3.7 billion in revenue, down slightly from the prior year.

However, profitability improved meaningfully, with gross margin expanding to 33.2%. Adjusted earnings per share came in at $1.41.

Perhaps most encouraging was the company’s cash generation: Operating cash flow for the quarter reached $956 million, and free cash flow totaled $883 million. For the full year, the company produced $688 million in free cash flow while continuing to reduce debt and streamline operations.

Now let’s turn to valuation.

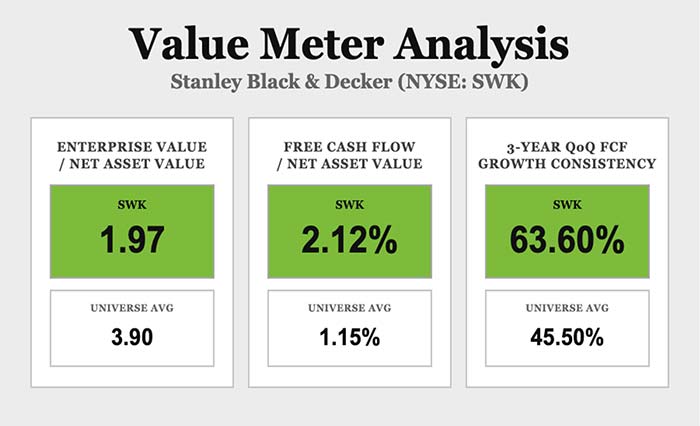

Stanley Black & Decker currently trades at an enterprise value-to-net asset value ratio of 1.97. That’s dramatically lower than the broad market average of 3.9. In other words, investors are paying about 49% less for each dollar of the company’s assets than they would for the typical business.

That kind of discount suggests the market still harbors doubts about the company’s recovery.

But asset prices alone don’t tell the full story. What really matters is how efficiently those assets generate cash.

Here, Stanley Black & Decker looks surprisingly strong. Its free cash flow-to-net asset value ratio stands at 2.12%, which is about 85% higher than the broad market average of 1.15%.

That tells us the company is converting its assets into cash more effectively than many of its peers.

Consistency also matters when evaluating a company’s cash engine. Over the past three years, Stanley Black & Decker’s quarterly free cash flow has increased from the previous quarter about 63.6% of the time. The broad market average sits closer to 45.5%.

That indicates a business with improving cash flow momentum.

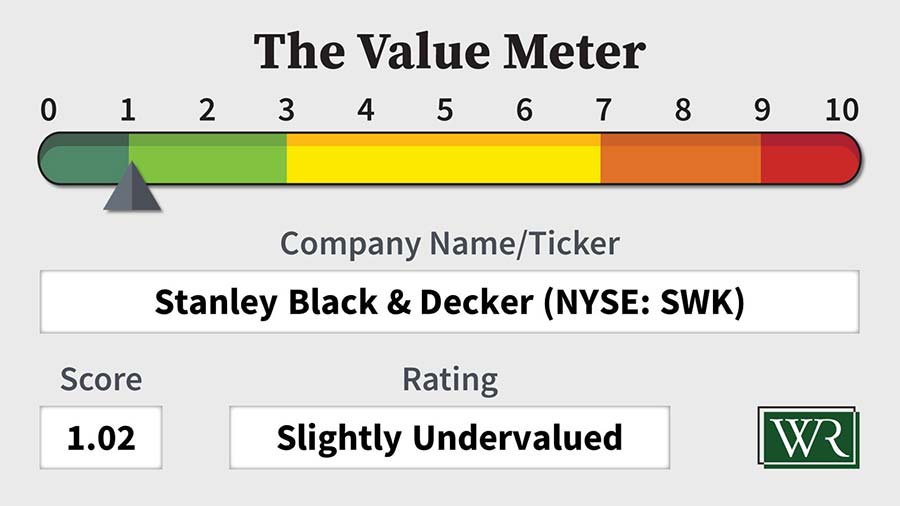

At first glance, Stanley Black & Decker may look like a slow-growing industrial name facing cyclical pressures. However, the numbers tell a more balanced story.

The stock trades at a steep discount to the broader market while displaying above-average cash flow efficiency and improving operational discipline. That combination suggests the market may be overly pessimistic about the company’s turnaround progress.

The Value Meter rates this one “Slightly Undervalued.”

What stock would you like me to run through The Value Meter next? Let us know in the comment section below.

{kind=link}